It’s Open Enrollment for Health Insurance. Am I a Small Business?

Open enrollment started today for the approximately 15 million people – less than 5% of the U.S. population – who do not purchase their health insurance through an employer, or receive it via a government-run program, such as Medicaid, Medicare, or military health care. Likewise, for people enrolled in Medicare, or many employer plans, it is the season to be making a choice about what health insurance you’d like to have for you and your family next year.

As a small business owner, I am also faced with a decision about whether and how to offer insurance to my employees, and what to offer. Here is where the fun begins and where my work life as a state health policy consultant collides with my experience as an employer trying to do the right thing.

In Virginia, as of 2018, I can now choose between buying coverage in the individual market or the small group market. This is because the Virginia legislature passed SB672 this summer, revising the definition of “small employer.” Here is the super boring, but very important change as described by the Virginia Bureau of Insurance in a bulletin to health insurance carriers:

The new law broadens the definition of “small employer” in §§ 38.2-3406.1 and 38.2-3431 of the Code of Virginia (“Code”) to include a “self-employed individual, and to allow a sole shareholder of a corporation or a sole member of a limited liability company (“LLC”), or an immediate family member of such sole shareholder or sole member, to count as an employee of the corporation or LLC, provided that the individual has performed a service for remuneration under a contract of hire.

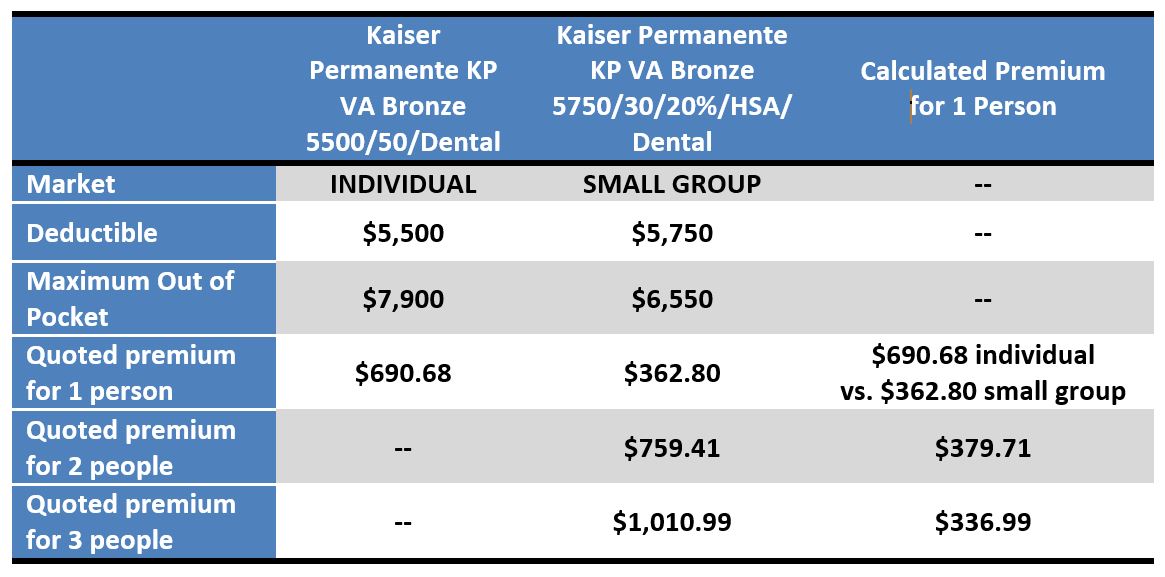

Why does this matter? Because the rates offered to me in the small group market are much lower than those offered to me in the individual market for the same coverage, in the same market, with the same selection of providers. The difference is stark as the table below shows.

Table 1. M2 Health Care Consulting Healthcare.Gov Individual v. Small Group Rate Comparison

Notably, the Virginia Bureau of Insurance admits in the summer bulletin, “the inclusion of sole proprietors in the definition of “small employer” does conflict with the definitions of “small employer” as administered by the Department of Health and Human Services, the Department of Labor, and the Internal Revenue Service, § 1321(d) of the Patient Protection and Affordable Care Act (“ACA”)…” [emphasis added]

But in its defense of possibly being in violation of federal law, Virginia argues first, that this provision “does not ‘prevent the application’ of the ACA,” and second, that other states have enacted similar laws.

Health care is confusing, expensive, and has become increasingly frustrating. Virginia decided to make a health care policy change this year that makes at least one small business less frustrated, while at the same time making health insurance options for me and my employees less expensive and we appreciate it. Let’s keep working on the system and see what else we can do!

Leave A Comment